You're probably dealing with one of two problems right now.

Either your business is growing and you need to know whether that next hire, equipment purchase, inventory buy, or contract will help cash or crush it. Or you're looking a few years ahead and realizing your company needs to perform well now and also look buyer-ready later. Most founders try to solve both problems with a budget. That's the wrong tool.

A financial forecast is what you use when you need decisions, not just spending limits. If you want to know how to create a financial forecast that helps you run the business, you need a model built for two jobs at once. It has to protect operational resilience when costs or collections move against you, and it has to support exit readiness if you may sell in the next few years.

Table of Contents

- Your Starting Point Why a Forecast Is Not a Budget

- Define Your Assumptions and Business Drivers

- Build a Connected Three-Statement Financial Model

- Stress-Test Your Model with Scenario Analysis

- Turn Your Forecast into a Management Tool

- When Your Spreadsheet Needs a Strategic Partner

Your Starting Point Why a Forecast Is Not a Budget

A budget is a target. A forecast is a decision tool.

That difference sounds small, but it changes how you run the company. A budget usually gets set once, then everyone spends the year comparing actuals against a plan that may already be outdated. A forecast should move as facts change. If a major customer slows payments, freight jumps, or backlog softens, your forecast should show the impact fast enough for you to act.

If you've only ever built an annual budget, start by dropping the idea that precision equals usefulness. A forecast isn't there to make you feel organized. It's there to answer questions like these:

- Can we afford this hire: before revenue fully lands?

- Can we take this job or contract: without creating a cash squeeze?

- Can we absorb a cost shock: without cutting somewhere else?

- Can this business support an exit story: that a buyer will believe?

If you need help separating the spending plan from the decision model, this guide on how to create a business budget is a useful companion. Keep the two tools separate. They solve different problems.

A budget sets limits and a forecast tests reality

Here's the cleanest way to think about it.

| Tool | Primary purpose | Best use |

|---|---|---|

| Budget | Set targets and spending guardrails | Annual planning and accountability |

| Forecast | Predict likely outcomes based on current facts | Cash decisions, hiring, pricing, borrowing, expansion, exit planning |

A founder who treats a forecast like a budget usually hides risk. A founder who treats a budget like a forecast usually changes direction too often. You need both, but the forecast should drive near-term operating decisions.

Practical rule: If your model doesn't change when your assumptions change, you're looking at a budget, not a forecast.

Match the forecast to the decision

Different decisions need different time horizons. Don't build a giant model when a narrower one would answer the specific question.

Use this shortcut:

- Short-term cash forecast: Best when payroll, vendor timing, tax payments, or project billing cycles are creating stress. Construction companies often need this first because revenue recognition and cash collection rarely move in sync.

- Operating forecast: Best for staffing, pricing, inventory, margin planning, and working-capital decisions. This is the model most founder-led businesses should maintain consistently.

- Strategic forecast: Best for expansion, debt capacity, acquisitions, ownership transition, or exit planning. With this forecast, you test whether the business can grow without becoming fragile.

Clean data comes before clever modeling

Founders often want to jump straight to projections. Don't. Start by cleaning the historicals.

A practical baseline for operating companies is at least 2–3 years of monthly historical results when possible, because that captures both trend and seasonality. In early-stage companies with limited history, a common starting point is a 12-month cash flow statement that gets refined as actual data comes in, according to this financial forecasting guidance.

Your historical data should include the basics:

- Income statement history with revenue, gross margin, payroll, overhead, and unusual items isolated.

- Balance sheet history so you can see receivables, payables, debt, inventory, and owner-related accounts clearly.

- Cash flow history that shows where cash really moved, not just where profit appeared.

- Operational support like backlog, pipeline, utilization, unit volume, collections timing, and purchasing patterns.

If the books are messy, fix classification issues before forecasting. Don't carry bad coding into a model and call it strategy.

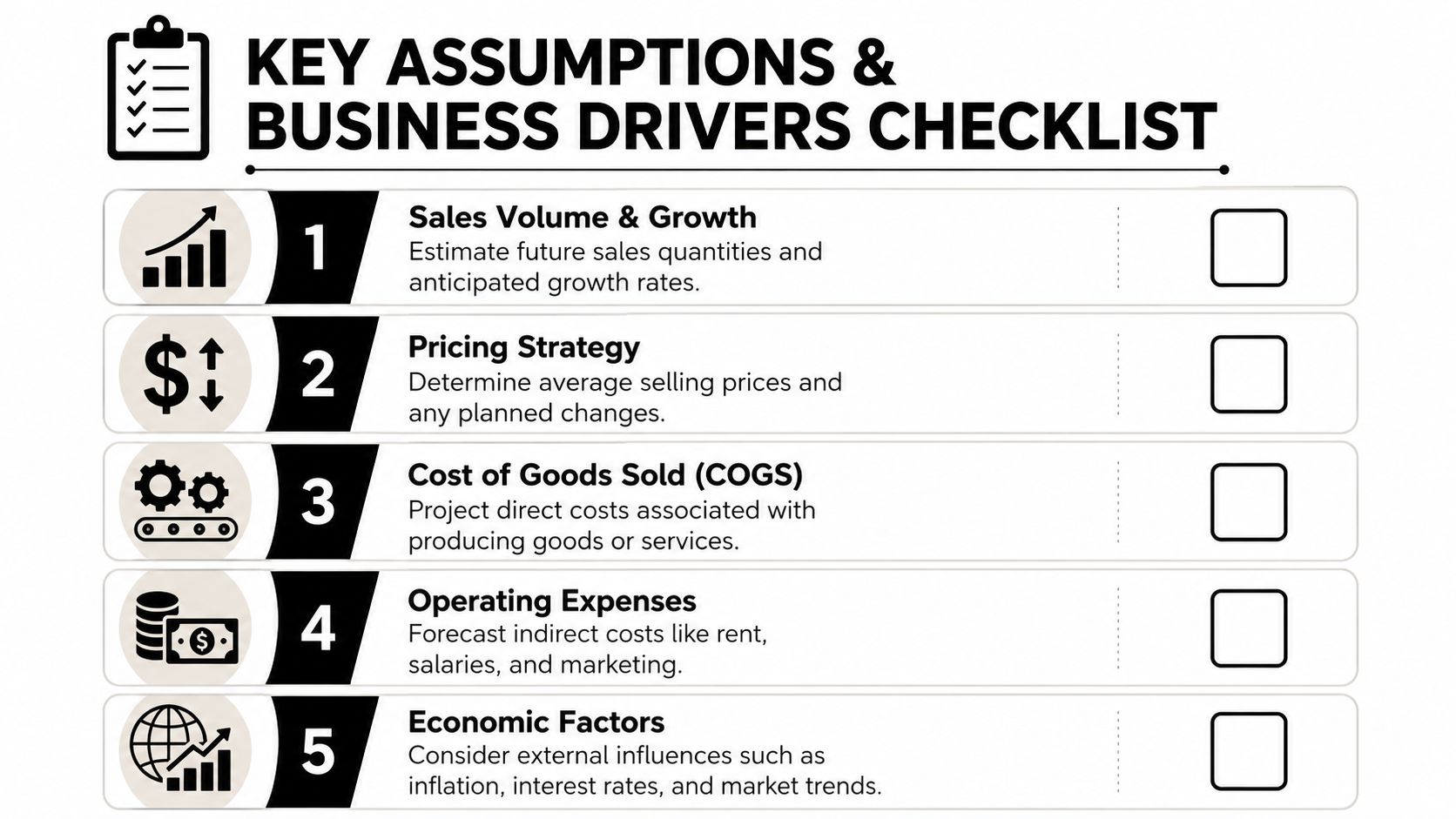

Define Your Assumptions and Business Drivers

Your forecast gets useful the moment it answers real operating questions.

If a key supplier raises prices, how much margin do you lose before cash gets tight? If demand softens for two quarters, which hires still make sense? If you want to sell the business in three years, which drivers will a buyer scrutinize first? Build your assumptions to answer those questions, not to fill a spreadsheet.

If you're building beyond an annual operating view, connect this work to a long-term financial planning process so your forecast supports both near-term decisions and multi-year strategy.

Start with operating drivers, not a revenue guess

Founders often begin with a top-line target and force the rest of the model to fit it. That approach produces pretty spreadsheets and weak decisions.

Start with the inputs that create revenue and cash flow. Revenue should come out of those inputs.

For example:

- Distribution business: units shipped, average order value, pricing changes, customer retention, freight recovery, vendor rebates.

- Construction company: backlog conversion, bid win rate, project start timing, labor availability, change orders, job mix.

- Professional services firm: billable headcount, utilization, realization, average billing rate, client concentration, project duration.

This gives your team something concrete to challenge. Your operations leader can question throughput. Your sales leader can challenge conversion timing. Your controller can pressure-test margin assumptions. That is how you improve a forecast.

Build assumptions around resilience, not just growth

A standard founder forecast asks, “How fast can we grow?”

A better one also asks, “What breaks first?”

Include the assumptions that expose operating fragility. If your business depends on materials, model input cost swings and lead-time changes. If labor is tight, model wage pressure, overtime, and lower productivity during ramp periods. If you carry inventory, model what happens when turns slow and cash gets trapped on the shelf.

These are not edge cases. They are the operating realities that separate a durable business from one that looks profitable until cash disappears.

Exit-readiness belongs here too. Buyers and lenders will focus on whether your performance comes from repeatable drivers or founder heroics. Build assumptions that show revenue concentration, margin by line of business, recurring versus project revenue, customer retention, and working-capital discipline. If your model cannot explain those drivers clearly, your valuation story will be weak.

Build an assumptions tab your team can challenge

Put every material assumption in one place. Do not bury inputs inside formulas across multiple sheets.

Your assumptions tab should include these categories:

- Revenue drivers: unit volume, pricing, backlog conversion, utilization, billable rate, project count, contract timing.

- Direct costs: labor mix, subcontractor usage, material input assumptions, production costs, freight, commissions.

- Operating expenses: headcount plan, salaries, rent, software, insurance, travel, marketing, owner compensation.

- Working capital: collections timing, inventory turns, vendor terms, retainage, deposits, prepaid expenses.

- Capital items: equipment purchases, lease commitments, maintenance spending, debt service.

Add notes beside each input that explain the source. A signed customer contract beats a hopeful pipeline estimate. A vendor quote beats a generic inflation placeholder. A hiring plan tied to named roles beats a round-number payroll increase.

Forecast assumptions should be traceable. If no one can explain where a number came from, it doesn't belong in the model.

A simple assumptions layout might look like this:

| Assumption category | Input | Basis |

|---|---|---|

| Sales | Units, projects, billable hours, pricing | Pipeline, backlog, signed work, recent trend |

| Gross margin | Material, labor, freight, subcontractor cost | Vendor quotes, labor plan, historical mix |

| Overhead | Headcount, systems, facilities, insurance | Hiring plan, contracts, renewal schedules |

| Working capital | Collection timing, payables timing, inventory needs | Actual aging, vendor terms, purchasing cycle |

Choose the few drivers that change decisions

You do not need a huge list of inputs. You need the handful that change what you would do next.

For construction, focus on backlog burn, labor efficiency, change order timing, and overbilling or underbilling. For distribution, focus on volume, pricing, gross margin by product line, freight, and collections timing. For professional services, focus on utilization, realization, staffing mix, and concentration risk.

Use one hard test. If a driver moves, would you hire differently, price differently, buy differently, borrow differently, or change your exit timeline? If yes, keep it in the model. If no, cut it.

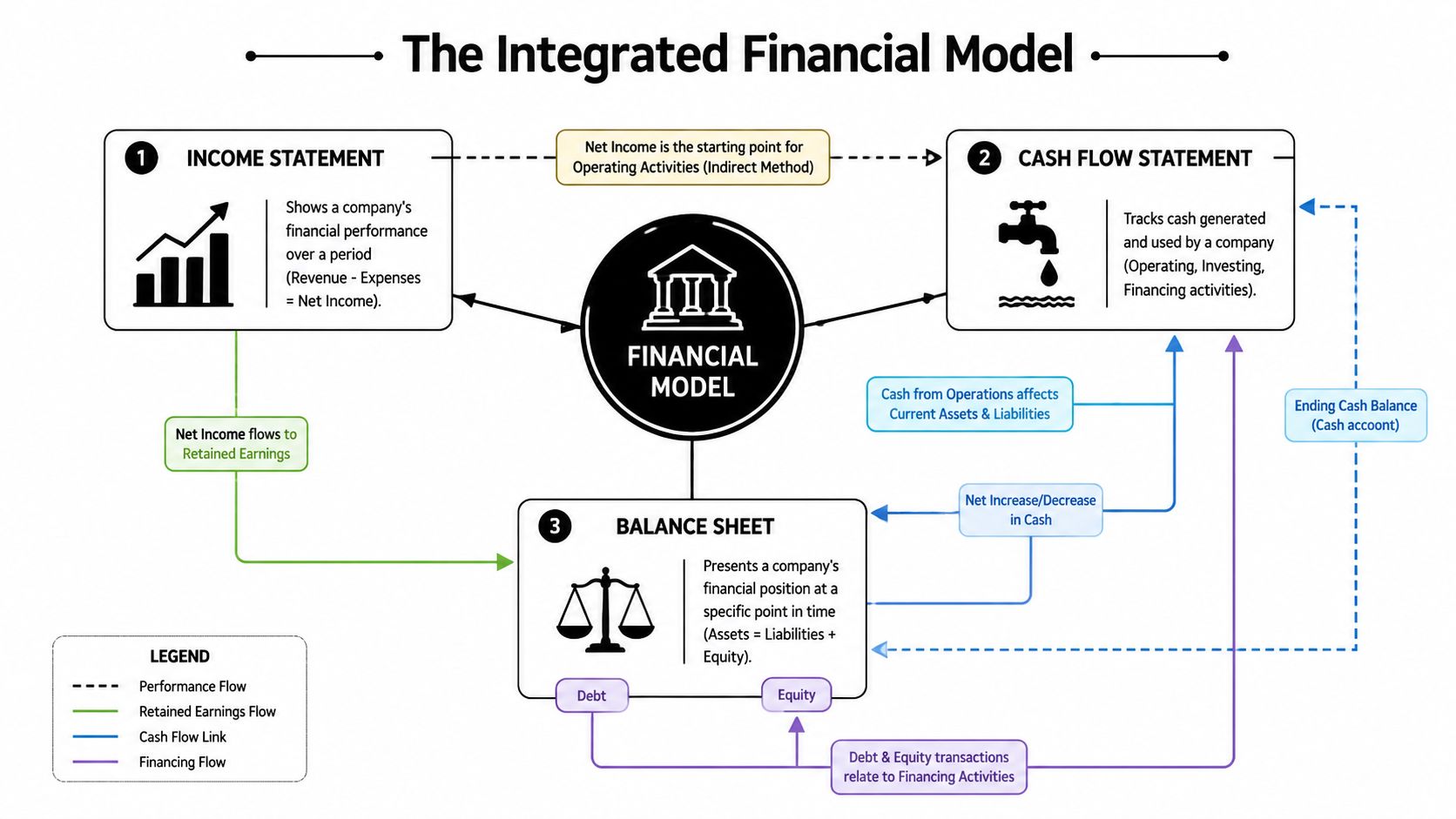

Build a Connected Three-Statement Financial Model

Many founders think the income statement is the forecast. It isn't. Profit without cash visibility is how businesses get blindsided.

A real operating forecast connects the income statement, balance sheet, and cash flow statement. That structure matters because lender-ready and investor-ready projections are built from assumptions, historical drivers, and these three linked statements, as outlined in OneStream's financial forecasting guidance.

Early in the build, it helps to visualize the system:

Treat the statements as one system

Think of the three statements this way:

- Income statement: shows whether operations produce profit over a period.

- Balance sheet: shows what the business owns and owes at a point in time.

- Cash flow statement: shows how cash moved through operating, investing, and financing activity.

If they don't connect, the model isn't reliable.

For a founder, the connection matters because most important decisions hit all three statements at once. Hiring affects payroll expense, accrued liabilities, and cash. Buying equipment affects cash, fixed assets, depreciation, and debt if financed. Landing a big customer affects revenue, receivables, cash timing, and working capital pressure.

Follow one transaction through the model

Take a simple example. You win a large project or order and invoice the customer.

On the income statement, revenue appears and gross profit follows based on direct costs. On the balance sheet, accounts receivable goes up if the customer hasn't paid yet. On the cash flow statement, cash doesn't increase immediately unless the customer pays. That's the part founders often miss. Revenue growth can create a cash problem when receivables build faster than collections.

Now take an equipment purchase.

The equipment doesn't hit the income statement all at once in the same way cash leaves the business. Cash goes out when you buy it. The asset lands on the balance sheet. Expense shows up over time through depreciation. If debt financed the purchase, principal and interest affect different parts of the model. That's why a one-sheet profit forecast won't answer a financing question properly.

Here's a simple way to check whether your model is wired correctly:

- Net income should flow into equity through retained earnings.

- Balance sheet accounts should drive working-capital movement in cash flow.

- Ending cash on the cash flow statement should match cash on the balance sheet.

- Debt balances should tie to principal repayments and new borrowing.

If one of those breaks, stop and fix it before adding more detail.

A quick visual walkthrough helps if this feels abstract:

What a lender or buyer expects to see

The point of the three-statement build isn't accounting elegance. It's credibility.

A lender wants to see whether debt service and working-capital demands can coexist. A buyer wants to see whether earnings convert to cash and whether growth requires constant owner intervention or heavy cash support. Your forecast needs to answer both.

A model that shows profit but can't explain cash is a storytelling problem. A model that explains both becomes a decision tool.

Keep the model readable. Use separate tabs for assumptions, calculations, outputs, and scenario controls. Label manual inputs clearly. Avoid hard-coded numbers in formulas. If you can't audit it quickly, you won't trust it under pressure.

Stress-Test Your Model with Scenario Analysis

Most founder forecasts fall apart when founders build one version of the future and pretend that's discipline.

It isn't. If your business operates in construction, distribution, or professional services, your margins can get hit by cost changes or delayed collections before the income statement gives you enough warning. The more useful question is not just how to create a financial forecast. It's how to create one that stays useful when conditions move against you.

Guidance for lender-facing forecasting makes this point clearly. Founders in volatile industries need to model sudden changes in costs and cash timing, including the very practical risk that margins can be erased by a 5% input-cost swing or a 15-day collections delay, as noted in this lender-oriented budgeting and forecasting article.

A simple story from a distribution business

A distributor I'd worry about usually looks healthy on the surface. Sales pipeline is solid. Orders are moving. Gross margin looks acceptable on average.

Then two things happen at once. Freight costs rise faster than expected, and a large customer stretches payment timing. Revenue may still look fine. Cash doesn't.

The founder now has a real management problem:

- Should they reduce inventory buys?

- Should they pause hiring?

- Should they push for price adjustments now or wait?

- Should they draw on a line of credit or preserve availability?

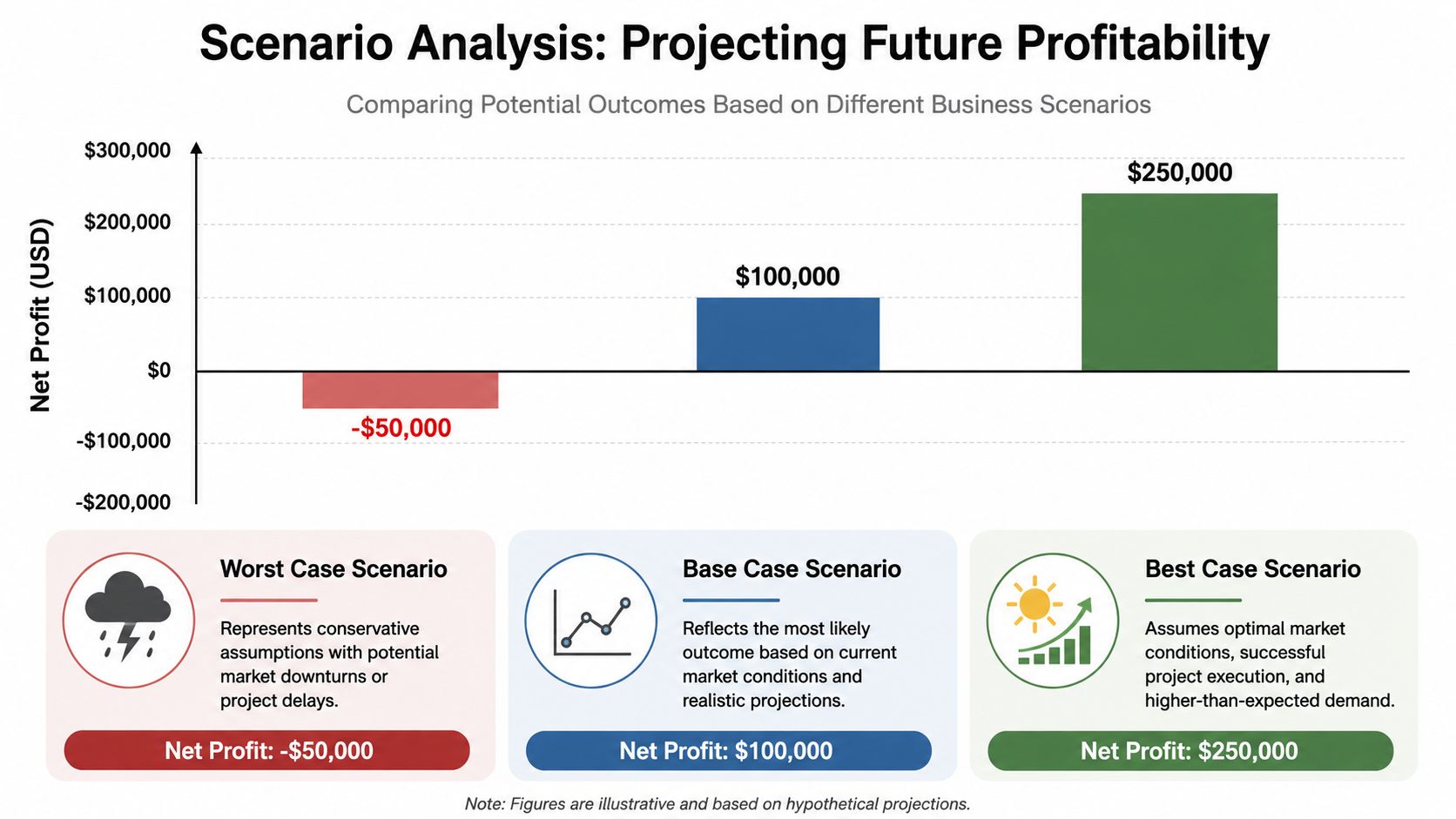

A single base-case forecast won't answer that. Scenario analysis will.

The scenarios that matter most

You don't need a dozen scenarios. Start with three and make them decision-oriented.

| Scenario | What changes | What decision it should trigger |

|---|---|---|

| Base case | Most likely assumptions | Normal staffing, pricing, purchasing |

| Downside case | Slower collections, cost pressure, delayed starts | Expense controls, cash preservation, pricing action |

| Upside case | Faster wins, stronger demand, better mix | Capacity planning, hiring timing, inventory support |

Then layer in specific sensitivities for the drivers that can hurt you fast.

For founder-led operating companies, I'd usually test these first:

- Input cost movement: materials, labor, freight, subcontractors.

- Collections timing: large customer delays, retention release, disputed invoices.

- Volume shifts: backlog timing, shipments, utilization, project starts.

- Gross margin mix: low-margin work crowding out better work.

- Capital strain: equipment needs, maintenance surprises, debt service pressure.

Don't label a scenario “worst case” unless you know what management will do in response. A scenario without actions is just anxiety in spreadsheet form.

Turn scenario outputs into decisions

Your output shouldn't stop at profit. It should show where you hit constraints.

Ask the model:

- When does cash get tight

- What operating levers can management pull

- Which assumptions hurt fastest

- What action happens automatically if a threshold is crossed

That last point matters. Good scenario planning creates pre-decisions. If collections slow beyond your acceptable range, maybe you freeze discretionary spending, tighten purchasing approval, or renegotiate vendor timing. If input costs move outside tolerance, maybe you reprice open bids or stop chasing low-quality work.

That's operational resilience. You're not waiting for month-end to discover the problem. You've already mapped the response.

Turn Your Forecast into a Management Tool

It's the second week of the month. Sales says demand is fine. Operations says labor is tight. Cash is lower than expected. You do not need another spreadsheet tab. You need a forecast review that forces a decision before the problem gets expensive.

A useful forecast changes how you run the business. It sets a cadence for pricing calls, hiring timing, purchasing limits, collections pressure, and capacity choices. It also gives you an early read on two things founders often miss until it's too late: how exposed you are to cost and cash volatility, and whether the business will look credible to a buyer.

Run a monthly review that ends with decisions

Hold one forecast meeting every month. Keep it short. Put the right owners in the room. Finance explains the numbers, but operators and sales need to own the actions.

A good review covers four points:

- Actual versus forecast: Where did results differ, and by how much?

- Driver changes: What changed in volume, price, labor efficiency, input costs, or collections?

- Forward effect: Does this issue wash out next month, or does it change the next two quarters?

- Decision and owner: What action gets taken now, by whom, and by when?

That last point matters most.

If gross margin slipped because freight and labor moved at the same time, decide whether you reprice new work, tighten quote approval, or cut low-quality jobs from the pipeline. If receivables stretched, assign the collection plan that day. If a hiring plan no longer fits cash, change it now instead of defending an outdated budget.

Use variance analysis to improve management judgment

Variance analysis is not an accounting exercise. It is how you train your leadership team to separate noise from a real operating problem.

Keep the review disciplined. Ask the same questions every time:

- Was the gap caused by timing, volume, price, cost, or mix?

- Is the issue temporary or repeating?

- Does the forecast need a new assumption, or does execution need correction?

- Did the miss create a cash risk, capacity risk, or margin risk?

Use a rolling forecast, not a static annual file. Extend the horizon each month so you are always looking ahead. As noted earlier, forecasting works better when assumptions are updated against actual results on a recurring basis. That is how you catch pressure from supplier increases, payroll creep, or slower collections before they turn into a funding problem.

Build management reporting with an exit lens

If you may sell your business in the next few years, your forecast needs to do more than help you survive the quarter. It needs to show a buyer that earnings are durable, cash conversion is real, and the company does not depend on you to hold every key relationship together.

That changes what you track.

Pull a small set of KPIs directly from the forecast and review them every month:

- Gross margin quality: Are you winning profitable work or filling capacity with weak jobs?

- Cash conversion: Are receivables and inventory turning into cash in a predictable way?

- Customer concentration: Would one account change the story too much?

- Owner dependency: Can the business keep performing without your direct involvement in every sale, approval, or escalation?

- Capital demands: How much ongoing equipment, systems, or working capital does the business need to sustain earnings?

A buyer will examine those patterns closely. Your forecast should already answer the questions they will ask. If M&A planning is becoming real, this guide on the role of fractional CFOs in business mergers and acquisitions shows how finance leadership helps turn a forecast into a sale-ready decision tool.

A buyer does not pay more because your spreadsheet looks polished. They pay more for a business that handles volatility, protects margin when costs move, converts profit into cash, and can run without founder heroics. That is what a management forecast should prove every month.

When Your Spreadsheet Needs a Strategic Partner

There's a point where a spreadsheet stops being a management tool and starts becoming a source of arguments.

You'll recognize it. Sales has one version. Operations has another. Accounting is trying to reconcile history while leadership debates assumptions that no one documented. The model grows, but clarity gets worse.

Signs you've outgrown a DIY model

You probably need outside strategic help when any of these are true:

- The model has become fragile: one broken formula changes everything and no one can audit it quickly.

- A major decision is on the table: expansion, debt, acquisition, ownership transition, or a large capital commitment.

- Cash and profitability are telling different stories: and leadership can't explain the gap.

- Exit planning is becoming real: but the forecast still reflects owner-centric operations instead of buyer-ready earnings.

- Meetings focus on whose number is right: instead of what management should do next.

In those moments, you don't need bookkeeping. You need judgment. A strategic finance partner can pressure-test assumptions, connect the model to operations, and translate outputs into actions the leadership team will take.

What a strategic finance partner actually changes

A strong fractional CFO doesn't just build a prettier file. They give the business a decision framework.

That usually means cleaner assumptions, tighter scenario design, better working-capital visibility, and clearer accountability in the monthly review cycle. It also means preparing the model for outside scrutiny. Banks, buyers, and boards all ask different questions. The model has to answer them cleanly.

If M&A or ownership transition is part of the picture, this overview of the role of fractional CFOs in business mergers and acquisitions is worth reading. It explains where strategic finance support becomes necessary, especially when the stakes move beyond routine planning.

AmbitionCFO is one example of a fractional CFO firm that works with founder-led companies on cash flow modeling, forecasting, KPI reporting, and exit planning. That kind of support fits when the business has outgrown a bookkeeper-level view of the numbers but doesn't need a full-time CFO.

If your forecast still lives as a static spreadsheet instead of a decision tool, it's time to fix that. AmbitionCFO works with founder-led businesses to build practical forecasting models tied to cash flow, margin, and exit readiness so you can make better operating decisions now and prepare for what comes next.