You're probably making growth decisions with partial information.

A department head wants to hire. Operations wants new equipment. Sales says demand is there. Your controller hands you last month's P&L, but that report only tells you what already happened. It doesn't tell you whether you can afford the next move, what happens if collections slow down, or whether the decision improves profit and cash at the same time.

That's where most founder-led companies get stuck. They have accounting. They don't have a real budget.

If you want to know how to create a business budget that helps you run a growth-stage company, stop thinking about it as an expense worksheet. A CFO-grade budget is a decision tool. It should help you test hiring plans, pressure-test margin, spot cash gaps early, and show whether your strategy is building enterprise value or just creating more complexity.

This matters even more if your business is already past the startup stage. For companies in the $10M to $100M range, simple spreadsheets and annual guesswork usually break down. You need an operating budget tied to business drivers, a cash flow forecast tied to timing, and a review process that forces accountability.

Your Business Budget Is More Than an Expense Sheet

A founder I talk to recently had a familiar problem. Revenue looked solid. The backlog was healthy. The leadership team wanted to add capacity. But no one could answer three basic questions with confidence.

Can we afford the hires before the revenue arrives?

Which business line funds the investment?

What happens if customer payments slip?

That's not a bookkeeping problem. That's a planning problem.

A basic budget tracks categories. A useful budget shows cause and effect. It connects sales activity to gross margin, gross margin to operating cost, and operating performance to cash. If your budget can't answer “what if we add a salesperson,” “what if a project starts late,” or “what if material costs rise,” it's incomplete.

A real budget should help you make decisions before the money is spent, not explain them after the fact.

For established businesses, especially in construction, distribution, and professional services, the right budget has three jobs:

- Guide operating decisions so hiring, purchasing, and pricing align with expected profit.

- Protect cash so growth doesn't create a liquidity problem.

- Support strategy so the business gets more scalable, more predictable, and more valuable.

That's the standard I recommend. Not a static annual file nobody opens after January. Not a wish list built around top-line optimism. A working financial model that management uses every month.

If you're serious about learning how to create a business budget, build one that reflects how your company operates. Revenue doesn't appear by magic. Expenses don't hit evenly. Cash never moves in perfect sync with profit. Your budget has to respect those realities or it will fail when you need it most.

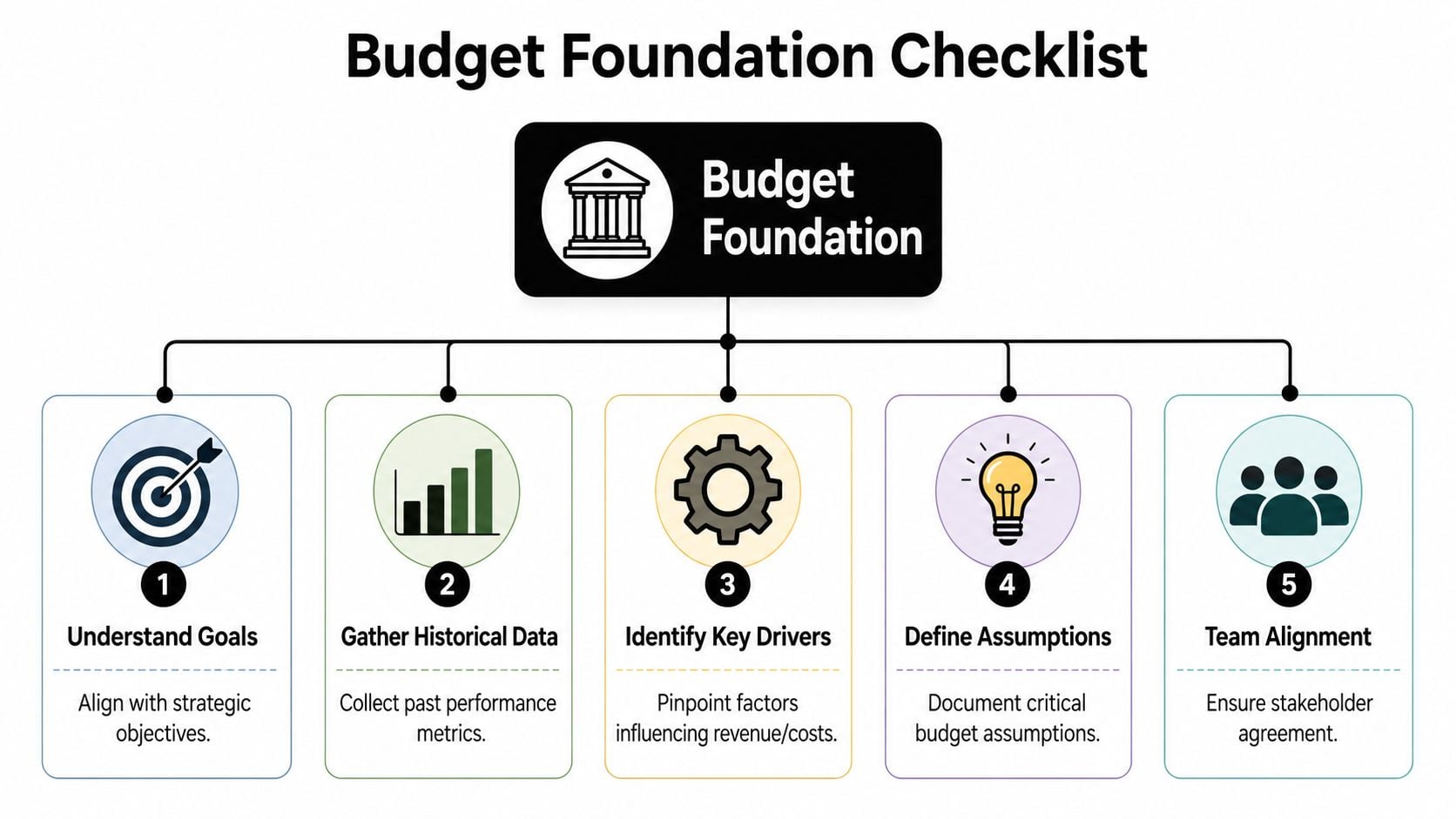

Lay the Foundation Before You Build the Budget

Most bad budgets fail before the spreadsheet opens. The inputs are weak, the assumptions are vague, and the revenue forecast is detached from reality.

That's why the first step isn't modeling. It's preparation.

A durable budget starts with history. A solid business budget should be built from at least 12 months of historical revenue and expense data, then stress-tested by separating fixed costs from variable costs before projecting profit and setting a contingency reserve, according to NerdWallet's business budgeting guidance.

Clean up the financial history first

If your historical data is messy, your forecast will be fiction.

You need clean monthly financials that reflect how the business operates. That means reclassifying one-off items, correcting coding errors, separating owner-specific spending from business spending, and making sure revenue and direct costs land in the right periods. If your statements are inconsistent, trend analysis becomes useless.

Focus on these records:

- Monthly income statements for at least the last full year, and preferably longer if seasonality matters

- Monthly balance sheets so you can spot working capital issues

- Cash flow history so you can see where profit and liquidity diverged

- Department, job, customer, or location detail if your business has multiple profit engines

If you don't trust the data, stop and fix that first. A polished budget built on bad accounting is still a bad budget.

Identify the real business drivers

Revenue is not a single line item. It's an output.

Founders often say, “We'll grow sales next year,” but that's not a forecast. A usable forecast has drivers behind it. You need to identify what creates revenue in your business, then model those drivers explicitly.

Here's what that looks like in practice:

| Business type | Stronger budgeting driver |

|---|---|

| Distribution | Active customers, order frequency, average order value, gross margin by product mix |

| Construction | Active jobs, bid conversion, schedule timing, average project margin |

| Professional services | Billable capacity, utilization, realization, client retention |

Budgeting ceases to be generic. A distribution company with flat order volume and better pricing behaves differently than one with more customers and lower margin. A construction firm with booked work but delayed starts has a cash timing issue even if backlog looks strong.

Practical rule: If the revenue line can't be explained by a handful of operating drivers, it isn't ready for budget use.

Break costs into the right buckets

Many organizations know fixed versus variable costs in theory. They apply it poorly in practice.

You need three buckets, not two:

- Fixed costs stay largely stable over the planning period. Think rent, core salaries, software subscriptions, insurance.

- Variable costs move with revenue or production. Think freight, materials, commissions, subcontract labor tied to job volume.

- Semi-variable costs have a base level, then rise when activity increases. Think warehouse labor, overtime, project management support, certain utilities.

That third category matters. Semi-variable costs are where growth-stage businesses get surprised. Revenue rises, and suddenly a “mostly fixed” department needs another manager, another coordinator, or more outsourced support.

A simple worksheet helps:

| Cost item | Type | What makes it move |

|---|---|---|

| Warehouse lease | Fixed | Contracted occupancy |

| Sales commissions | Variable | Revenue closed |

| Project coordinator labor | Semi-variable | Number of active jobs |

| Fuel and delivery costs | Variable | Shipment volume and routes |

| ERP subscription | Fixed | Contract terms |

| Temporary labor | Semi-variable | Capacity gaps and seasonality |

Write down assumptions before anyone argues about numbers

A budget should never hide assumptions. It should expose them.

Document the core assumptions behind the model. Pricing changes. hiring timing. expected backlog conversion. planned capital spending. collections pattern. major customer risk. If you don't write these down, every budget meeting turns into a debate over memory and opinion.

For strategic planning, tie those assumptions to the broader roadmap. If you're budgeting in support of expansion, ownership transition, or margin improvement, your operating plan should match your longer horizon. That's the difference between annual budgeting and actual financial leadership. If you're planning beyond the next budget cycle, pair this work with a long-term financial plan.

Construct Your Driver Based Operational Budget

Once the foundation is solid, build the operating budget from the ground up. Don't use the lazy method of taking last year and adding a hopeful increase. That approach hides risk, ignores operational reality, and tells managers nothing about what they're responsible for.

A practical way to create a business budget is to start with the last 12 to 24 months of revenue and expense history, then project income before setting spending limits, because budgeting is an estimate of projected income, fixed and variable expenses, and profit goals, as noted in Bob's Bookkeepers' budgeting guide.

Start with revenue mechanics, not hope

Revenue should be built from the business model upward.

Take a distribution company. Instead of writing “sales up next year,” break revenue into operating parts:

- Active customers

- Average order frequency

- Average order value

- Product mix or gross margin profile

The formula is simple: active customers × order frequency × average order value.

That model is far better than a top-line guess because management can influence each piece. Sales can drive account growth. Customer success can improve reorder behavior. Pricing discipline can protect value per order. Operations can monitor whether product mix is helping or hurting margin.

For a services firm, the structure changes. Revenue may be driven by billable headcount, utilization, rates, and collections timing. For construction, it may depend on awarded jobs, project schedule, percent complete, and change order assumptions. The principle stays the same. Build revenue from actions and constraints you can observe.

Layer in direct costs and gross margin logic

After revenue, model cost of goods sold or direct delivery costs. Here, many budgets become too blunt.

If your gross margin changes by customer type, service line, or product category, your budget should reflect that. Don't assume every dollar of revenue carries the same profitability. It rarely does.

Use questions like these:

- Are some customers heavier on service and lighter on margin?

- Do certain jobs require more subcontracted labor?

- Does your product mix shift seasonally?

- Are expedited freight or rush orders common in certain months?

A budget that captures gross margin behavior gives you something far more useful than expense control. It gives you a profitability forecast.

The fastest way to destroy a budget is to treat all revenue as equally good revenue.

Add operating expenses in the order they actually hit the business

Once you've forecast revenue and direct costs, build the rest of the P&L in layers.

Start with stable overhead. Then add capacity investments. Then add discretionary spend. Founders often do this backward. They start with what they want to spend, then hope sales support it. That's not budgeting. That's rationalized spending.

A stronger operating build looks like this:

Core fixed overhead

Rent, base salaries, software, insurance, recurring admin costs.Semi-variable support costs

Shipping support, project admin, overtime, outsourced operations help, temporary labor.Growth investments

Planned hires, market expansion spending, equipment, systems upgrades.Owner decisions and strategic projects

New initiatives, restructuring costs, readiness work tied to succession or exit.

This sequencing matters because it shows what the business must cover before discretionary investment. It also clarifies the break between “required to operate” and “chosen to grow.”

Build the budget by month

Annual totals hide too much. Use monthly periods.

A monthly budget reveals seasonality, hiring timing, payroll burden changes, bonus patterns, rent steps, and large recurring obligations. It also forces management to think about when actions happen, not just whether they happen.

Here's a practical checklist for a monthly operating budget:

- Revenue by month based on driver assumptions

- Direct costs by month based on expected mix and activity

- Headcount changes by month based on actual start dates

- Recurring overhead by month from contract and payroll records

- One-time items by month such as software implementation or equipment purchases

- Profit target by month so you can spot when the plan drifts

Build accountability into the model

Each major line in the budget should have an owner.

Sales should own the assumptions behind volume, mix, and pricing. Operations should own labor efficiency, production support, and fulfillment-related spending. Department leaders should own discretionary spend. Finance should own model integrity and reporting.

That's what turns a budget into a management tool rather than a finance exercise.

If no one owns the assumptions, no one owns the outcome.

Master the All Important Cash Flow Forecast

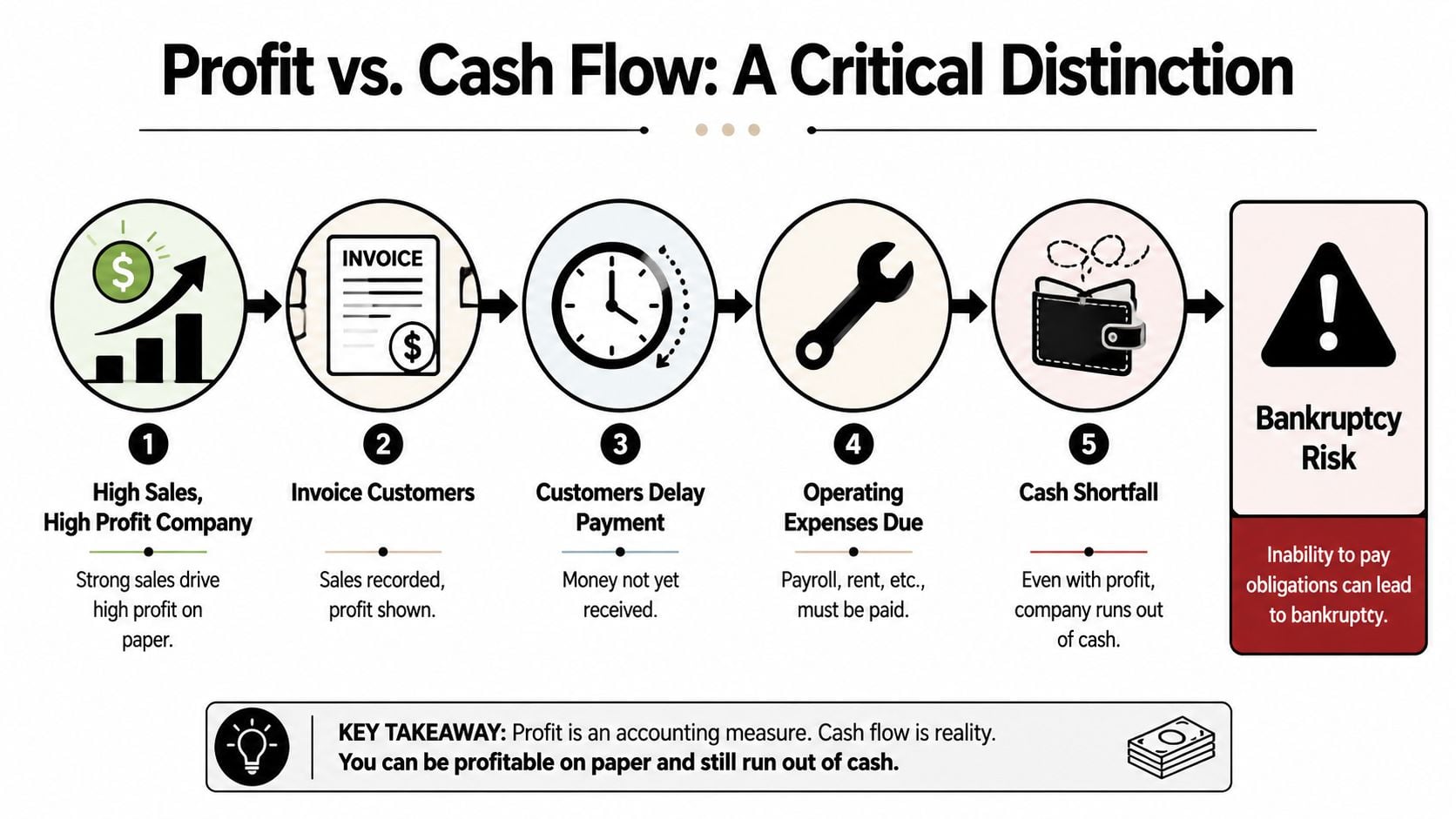

A profitable company can still run out of money. That's not unusual. It's what happens when timing gets ignored.

You book revenue. You issue invoices. Customers pay late. Payroll clears on schedule. Vendors want their money. Tax payments hit. Debt service hits. Suddenly the company shows profit on paper and stress in the bank account.

That's why a P&L budget alone isn't enough.

For businesses with volatile or project-based revenue, like construction or professional services, a standard P&L budget is not enough. Guidance emphasizes conservative revenue baselines and cash-flow overlays to manage cash timing risk, seasonality, and collections delays, according to Luca's budgeting guidance for small business.

A visual makes the issue obvious.

Profit and cash are different systems

Your income statement recognizes activity. Your cash flow forecast tracks movement of money.

That difference matters most in businesses with delayed collections, inventory purchases, project mobilization costs, or uneven billing. You can have a strong month operationally and still create a liquidity squeeze if cash receipts arrive after cash obligations.

The right response is to build a cash flow forecast on top of the operating budget.

That means taking the P&L assumptions and adding timing:

- When customers pay

- When vendors get paid

- When payroll clears

- When debt, tax, and capital expenditures hit

- When owner distributions are expected

Here's a useful primer before you model your own process:

Model the timing assumptions explicitly

Two terms matter here.

Days Sales Outstanding (DSO) is the average time it takes to collect from customers after invoicing.

Days Payable Outstanding (DPO) is the average time your business takes to pay vendors.

You don't need a theoretical finance lecture. You need practical assumptions. If customers usually pay slower than contract terms, use reality. If your team tends to pay key vendors early to preserve relationships, reflect that too.

A cash flow overlay usually includes:

| Cash driver | What you need to estimate |

|---|---|

| Customer collections | Payment timing by customer type or billing pattern |

| Vendor disbursements | Payment timing by supplier group |

| Payroll | Gross payroll timing, taxes, benefits |

| Debt service | Required principal and interest dates |

| Capital spending | Deposit timing and final payment timing |

| Taxes | Expected payment periods |

Conservative planning matters particularly when revenue is volatile. If revenue is volatile, don't budget cash as if every invoice will be paid promptly. That's how founders walk into preventable cash squeezes.

Budget revenue with ambition if you want. Budget cash with discipline.

Use a short-range cash tool for weekly control

For day-to-day liquidity management, I strongly prefer a 13-week cash flow model.

It forces weekly visibility into receipts, disbursements, payroll runs, debt obligations, and short-term risk. That's especially useful when the business is scaling quickly, dealing with project timing swings, or recovering from margin pressure.

A weekly model helps you answer questions like:

- Which week is the tightest for cash?

- What happens if a large receivable slips?

- Can we fund a hire before collections catch up?

- Do we need to delay capital spending or renegotiate payment timing?

For companies that need hands-on support, some firms provide this as part of fractional CFO work. For example, AmbitionCFO offers 13-week cash flow modeling, margin analysis, forecasting, and KPI reporting for founder-led businesses.

If rapid growth is straining working capital, this is exactly where hidden financial pressure shows up first. A strong forecast will expose it before the bank balance does. For more on that problem, review the hidden costs of rapid business growth.

Build cash reserves into the plan

A budget without a buffer is fragile.

If your revenue is project-based, seasonal, or concentrated among a few customers, assume timing will disappoint you at some point. A reserve gives management room to act instead of react. It also keeps one delayed payment from turning into a payroll crisis.

Cash planning isn't fear-based. It's operating discipline. The companies that stay in control aren't the ones with the prettiest P&L. They're the ones that can see cash trouble early and respond before options narrow.

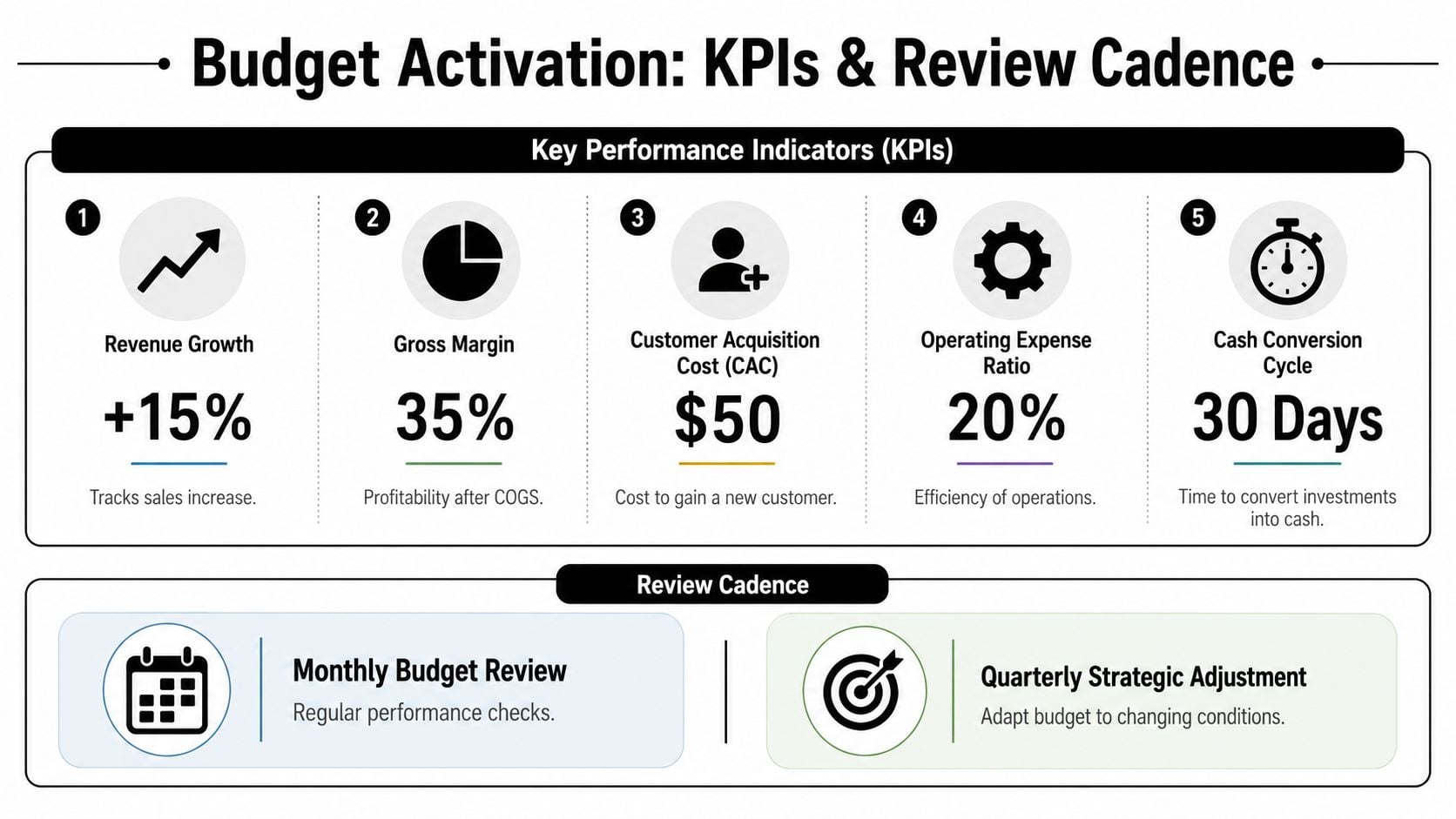

Activate Your Budget with KPIs and a Review Cadence

Most budgets die from neglect, not design.

The file gets approved, saved, and ignored until the year is half gone. By then, the misses are obvious, the cash pressure is real, and management is reacting instead of steering. If you want a budget to matter, tie it to a short list of operating metrics and review it every month.

Modern budgeting guidance recommends focusing on the 5 to 10 most important financial metrics and using a monthly review cadence to compare actual spending against plan and make adjustments, according to Budgetly's guide to building a business budget template.

Pick KPIs that explain budget performance

Don't track everything. Track what drives outcomes.

The right KPI set depends on the business model, but it should always connect directly to the budget. If a metric doesn't help explain a major revenue, margin, or cash result, it probably doesn't belong in the core dashboard.

Useful examples include:

- Gross margin when mix, pricing, or delivery efficiency determine profit

- Backlog quality when future revenue depends on project conversion and schedule reliability

- Utilization and realization for professional services firms

- Client or job profitability when some revenue creates more complexity than return

- Cash conversion indicators when working capital is under pressure

If you need a tighter scorecard, this overview of financial metrics every business owner should track is a practical starting point.

Run a real budget versus actual process

A proper monthly review meeting is not a ceremonial readout of reports. It's a management session.

Keep it focused. Use current-month actuals, year-to-date actuals, budget, and a current forecast. Then ask why the gap exists and what management will do next. That's the entire job.

A useful agenda looks like this:

| Topic | What management should answer |

|---|---|

| Revenue variance | Was the miss volume, pricing, timing, mix, or execution? |

| Gross margin variance | Did labor, materials, freight, subcontracting, or discounts move? |

| Operating expense variance | Which costs were intentional, which were sloppy, which are recurring? |

| Cash impact | Did the variance affect collections, payables, or near-term liquidity? |

| Forecast update | Does the remainder of the period need to change? |

Focus on variance diagnosis, not blame

Variance analysis is where the budget becomes operationally useful.

“Over budget” isn't a diagnosis. It's a symptom. You need to identify the actual driver behind the gap. Revenue may be behind because project starts slipped, not because the sales team underperformed. Margin may be down because customer mix changed, not because pricing failed. Labor may be high because rework increased, not because managers overscheduled.

Strong budget reviews ask “why did this happen?” and “what changes now?” They don't stop at “we missed.”

This process works best when department leaders participate. Sales, operations, and finance should all be in the room. The budget belongs to the business, not just the accounting team.

Reforecast while the year is still salvageable

A monthly review without reforecasting is incomplete.

If conditions change, update the outlook. Don't cling to the original plan just because it was approved. A budget is useful when it helps management adapt while there's still time to improve the result.

That's what turns budgeting into a control system. You're no longer recording history. You're using current information to protect margin, cash, and execution.

Use Strategic Budgeting for Growth and Exit Planning

Most owners underuse the budget. They treat it as a cost-control document when it should be a strategy document.

If your only budgeting question is “how do we keep spending in line,” you're leaving value on the table. The better question is this: what choices does the budget help you make about growth, risk, and eventual transition?

For founder-led firms, budgeting needs to support not just cost discipline but also valuation drivers for an exit. That includes connecting budget decisions to margin improvement, KPI design, and demonstrating recurring cash flow to prepare for a transition, according to Mowery & Schoenfeld's guidance on business budgeting.

Use scenarios instead of one story

A single forecast is fragile. Build at least three views of the future:

- Most likely reflects the operating plan you expect to execute

- Best case shows what happens if sales, margin, and execution outperform

- Downside case shows what happens if demand softens, projects slip, or collections slow

This isn't an academic exercise. It helps you decide when to hire, when to delay capital spending, whether to expand into a new market, and how much liquidity you need if conditions turn against you.

A strategic budget should answer questions like these:

- If we open a new location, when does it pressure cash?

- If we add senior talent, when does the margin benefit show up?

- If one large customer slows, what gets cut first?

- If we want to exit within the next several years, which metrics need to become more predictable now?

Budget for value creation, not just control

Buyers care about quality of earnings, predictability, and independence from the owner. Your budget should help improve all three.

That means using the budget to strengthen recurring cash flow, improve visibility into client or job profitability, and reduce reliance on founder intuition. The stronger your forecasting discipline, the easier it is to explain the business during diligence. Clean assumptions, consistent reviews, and a history of managing to plan make the company easier to understand and easier to trust.

That trust matters.

A business with disciplined forecasting usually presents as more stable, more scalable, and less dependent on heroic owner intervention. That's exactly the profile many owners want before a transition, whether the goal is internal succession, outside sale, or private equity recapitalization.

Ask the right strategic questions

At the senior level, budgeting should force decisions like:

| Strategic issue | Budget question |

|---|---|

| Expansion | Which investments create growth without breaking cash flow? |

| Succession | Can the business hit plan without the owner driving every decision? |

| Margin improvement | Which customers, jobs, or services deserve more capital and attention? |

| Exit readiness | Does the forecast show predictable profit and recurring cash generation? |

If your budget doesn't help with those questions, it's too narrow.

Turn Your Financial Story Into Your Strategic Advantage

A strong budget changes how you run the company.

Instead of reacting to last month's numbers, you start making decisions with forward visibility. You know what drives revenue. You know which costs scale and which ones don't. You know where cash gets tight. You know whether the plan supports growth, protects margin, and moves the business toward a more valuable future.

This is how to create a business budget. Start with clean history. Build from operating drivers. Layer in cash timing. Review performance monthly. Reforecast when reality changes. Use the budget to improve the business, not just explain it.

This is what founders want, even if they don't phrase it that way. They want clarity, confidence, and control. A CFO-grade budget gives them all three.

If your company has outgrown basic spreadsheets and backward-looking reports, it's time to build a planning system that matches the complexity of the business you've created.

If you want help building a budget that supports growth, cash flow control, and eventual exit readiness, contact AmbitionCFO. Their fractional CFO work is built for founder-led companies that need stronger forecasting, tighter financial visibility, and a budget that drives decisions.