You're probably feeling this already. Revenue is up, the team is bigger, payroll is heavier, and the business looks healthy on paper. But every major decision still feels harder than it should. Can you hire ahead of growth? Can you buy the equipment? Can you survive a delayed project, a slow-paying customer, or a margin squeeze without choking cash?

This is the reason to build a financial plan for small business when you're running an established company. At the $10M to $100M stage, this is no longer a lender document or a startup exercise. It's your operating manual. It tells you what the business can fund, where cash gets trapped, which growth bets are smart, and whether you're building a company that someone will want to buy someday.

Table of Contents

- Lay the Foundation for Your Strategic Financial Plan

- Build Your Core Forecasts Revenue Expenses and Cash Flow

- Turn Your Forecast into a Dynamic Decision-Making Model

- Establish Your KPIs and Reporting Rhythm

- Implement Systems Controls Risks and Advanced Strategy

- Your Next Step From Plan to Profit

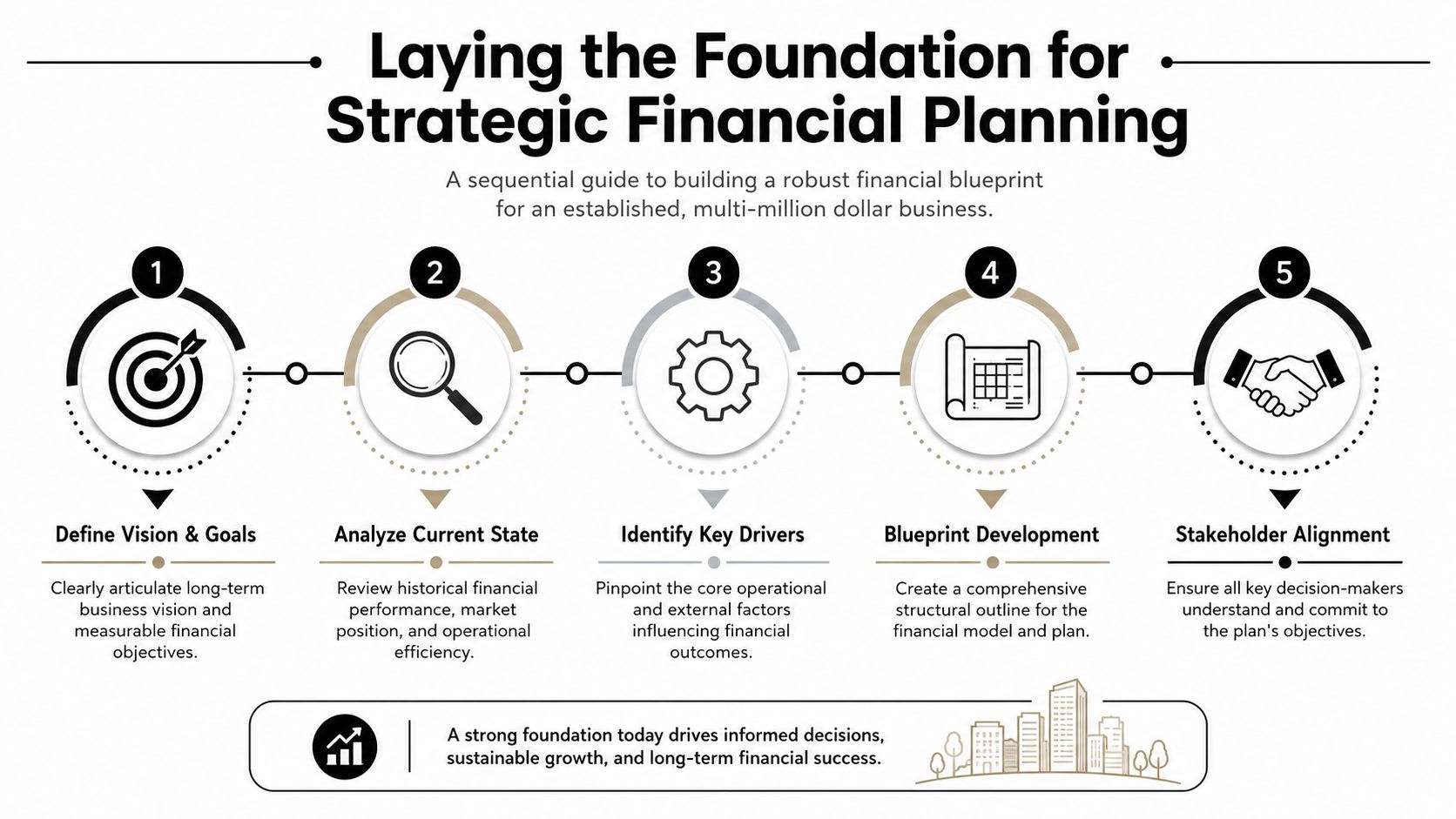

Lay the Foundation for Your Strategic Financial Plan

A good financial plan for small business starts with one question. What decision is this plan supposed to improve? If you can't answer that clearly, you'll end up with a spreadsheet that looks impressive and helps nobody.

For an established company, the answer usually falls into one of a few buckets. Growth. Risk control. Debt capacity. Ownership transition. Exit timing. If you say you want to “grow profitably,” that's too vague. If you say you want to open a second location, acquire a competitor, reduce owner dependence, or prepare the company for a sale in a defined time window, now you're planning around reality.

Start with the decision the plan must support

Your financial plan should tie directly to strategy. If your long-term objective is an exit, the plan needs to show how profit quality, cash generation, management depth, and capital needs improve over time. If your objective is expansion, the plan needs to show whether the business can fund that expansion internally or whether debt will strain liquidity.

Practical rule: Build the plan backward from the decision, not forward from a template.

That changes the discussion fast. Instead of asking, “What should my revenue grow to?” ask, “What level of cash flow and margin stability do I need before I add another crew, another sales rep, or another warehouse?”

The U.S. Small Business Administration business plan guidance is more useful here than most owners realize. The SBA treats the financial plan as a multi-year operating document, recommends forecasting the next five years, and calls for quarterly or even monthly projections for the first year. It also says a complete plan should include forecasted income statements, balance sheets, cash flow statements, and capital expenditure budgets, built on the last three to five years of historical statements.

That's the right framework for a mature company. You're not creating a static annual budget. You're building an operating model tied to strategy.

Set a real planning horizon

Most owners think in one of two bad extremes. Either they look only at next month's bank balance, or they create a distant growth vision with no operating bridge in between.

Use both horizons:

- First year: Monthly or quarterly detail. Execution relies on this.

- Years ahead: A broader five-year view. This view informs capital allocation and ownership decisions.

Your first year should answer practical questions such as:

- Hiring timing: Which roles need to be added, and when can cash support them?

- Capacity constraints: Will revenue stall because operations can't deliver?

- Capital spending: Which equipment purchases are mandatory versus optional?

- Debt obligations: What does repayment do to flexibility?

Your longer-range plan should answer bigger questions:

- Exit readiness: Is the company becoming less dependent on the owner?

- Valuation quality: Are margins, systems, and reporting becoming more reliable?

- Expansion logic: Does growth improve the business, or just make it more fragile?

Pull the right historical data before you forecast

Most forecasting errors start here. Owners try to build the future from memory, instinct, and one decent month.

Don't do that. Pull clean history first.

At minimum, gather:

- Profit and loss statements: Monthly detail for the past three to five years if available.

- Balance sheets: Monthly snapshots, not just year-end reports.

- Cash flow history: Bank movement and operating cash patterns.

- Aging reports: Accounts receivable and accounts payable.

- Sales detail: By customer, product line, service line, location, or job.

- Gross margin detail: By job, client, crew, route, or project type.

- Payroll detail: Fixed salary, overtime patterns, bonus structures.

- Capital spending history: Equipment, software, leasehold improvements.

Here's the organizing principle. Your chart of accounts matters less than your economic drivers. A contractor should be able to see margin by job. A distributor should see margin by customer and product category. A professional services firm should see realization, utilization, and client profitability.

Historical financials are not just records. They're evidence. Use them to prove what actually drives cash and profit in your business.

If your data is messy, fix the structure before you build the model. Standardize account names. Separate owner-specific expenses. Reclassify one-time items. Clean up job-cost coding. Tag revenue streams properly. The cleaner the history, the faster you can build a forecast that management will trust.

Build Your Core Forecasts Revenue Expenses and Cash Flow

Now you build the engine. At this point, most financial plans either become useful or turn into fiction.

A real financial plan for small business has three core forecasts that work together. Revenue. Expenses. Cash flow. Owners tend to focus on the first one because it's exciting. Lenders focus on the third one because it keeps them safe. You need all three, but cash flow deserves the most attention.

A frequently cited U.S. Bank statistic says 82% of businesses fail due to cash flow problems and poor financial planning, which is why strong planning focuses on month-by-month cash flow forecasts for at least 12 months and maintaining three to six months of operating expenses in reserve, as noted in Rippling's summary of business financial planning.

Forecast revenue from operations not hope

Don't forecast revenue by taking last year and adding a percentage. That's lazy, and it hides risk.

Build revenue from the ground up using the actual mechanics of your business:

- Construction firms: Start with backlog, close probability on bids, project start dates, production schedule, and crew capacity.

- Distributors: Start with customer demand patterns, pricing, order frequency, product mix, inventory availability, and sales rep capacity.

- Professional services firms: Start with active clients, pipeline, billable capacity, utilization, realization, and project timing.

If you have recurring revenue, separate it from project or one-time revenue. If you have seasonal swings, reflect them explicitly. If one large customer distorts the picture, isolate that customer and model them independently.

A good revenue forecast answers three questions:

- Where will the revenue come from?

- When will it be earned?

- When will it turn into cash?

That third question is where many owners get burned. Booked revenue isn't bankable cash.

Separate costs that move from costs that sit there

Once revenue is built, forecast expenses in two piles. Variable costs and fixed costs.

Variable costs rise or fall with activity. Materials, subcontractors, commissions, freight, direct labor in some models. Fixed costs sit there whether sales come in or not. Salaries, rent, software, insurance, debt service, core admin.

That separation matters because it lets you test margin under pressure. If revenue slips, which costs move down naturally? Which ones don't budge?

Use your historical data to map this clearly:

| Cost Category | Behavior | Management Use |

|---|---|---|

| Direct materials or direct project costs | Moves with sales or production | Protect gross margin |

| Commissions and incentive comp | Usually tied to volume or collections | Align selling with cash |

| Core payroll and rent | Mostly fixed in the short term | Measure operating leverage |

| Equipment or software commitments | Fixed once committed | Time purchases carefully |

| Discretionary spend | Adjustable | Create a fast response lever |

If your overhead has crept up, don't bury it in a broad SG&A line. Break it out. Owners need to see what they can control.

For budgeting discipline, this is also a good time to tighten your spending process. A simple operating budget with accountable line owners goes a long way. If you need a clean starting point, use this guide on how to create a business budget and adapt it to your departments or locations.

Build the cash flow forecast month by month

This is the part that keeps businesses alive.

Your cash flow forecast should run month by month for at least the next 12 months. Not quarterly. Monthly. In some businesses, weekly is even better for internal management, but monthly is the minimum for the strategic plan.

Keep the model simple enough to use:

| Item | Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Beginning cash | ||||||||||||

| Cash receipts from customers | ||||||||||||

| Other cash inflows | ||||||||||||

| Total cash in | ||||||||||||

| Payroll | ||||||||||||

| Direct costs and suppliers | ||||||||||||

| Rent and occupancy | ||||||||||||

| Debt payments | ||||||||||||

| Capital expenditures | ||||||||||||

| Taxes and other obligations | ||||||||||||

| Total cash out | ||||||||||||

| Net cash movement | ||||||||||||

| Ending cash |

The key is not the template. The key is the assumptions behind it.

Use realistic collection timing. If your largest customers tend to pay late, model that. If payroll is fixed and receivables are lumpy, model that. If inventory has to be bought before the sales show up, model that. If taxes hit in specific periods, model that.

Profit doesn't pay payroll. Cash does.

Once you've built the monthly forecast, compare ending cash to your reserve target. If you can't maintain a cushion of three to six months of operating expenses under your current plan, your growth strategy is probably too aggressive, your debt structure is wrong, or your collections process needs work.

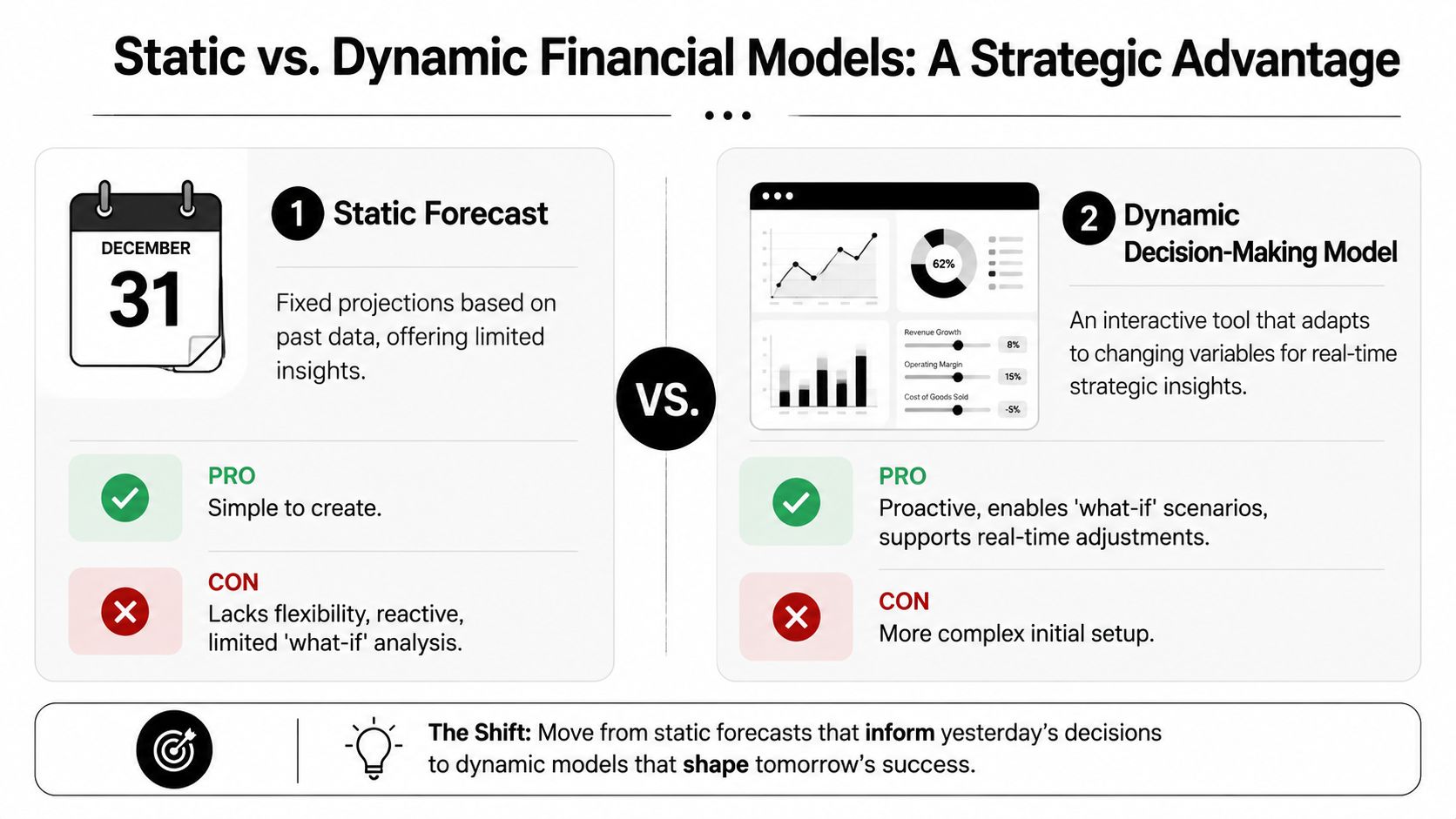

Turn Your Forecast into a Dynamic Decision-Making Model

A static forecast tells you what you hope happens. A dynamic model tells you what happens if reality shows up.

That difference matters because over-optimistic forecasting is one of the most common planning failures. The U.S. Chamber article on why small businesses fail notes that nearly half of startups fail within five years, with weak cash control frequently involved, and emphasizes stress-testing downside scenarios for slower collections and higher overhead. Even though you're not running a startup, the lesson still applies. Optimism breaks models faster than bad math.

Build three views of the business

You don't need a fancy system to do this. A solid spreadsheet model can handle it if the assumptions are clear.

Run the business through three scenarios:

- Base case: What you believe is most likely.

- Best case: What happens if sales convert faster, margins hold, and collections stay healthy.

- Worst case: What happens if revenue is delayed, gross margin slips, and customers pay slower.

These scenarios should not just change revenue. They should also change timing, margin, overhead pressure, and capital needs. That's where owners make mistakes. They cut sales in the downside case but forget that indirect labor, rent, software, and debt costs are still there.

Here's a practical set of variables to toggle:

| Driver | Base Case | Best Case | Worst Case |

|---|---|---|---|

| Sales close timing | Expected timing | Faster conversion | Delayed conversion |

| Collections | Normal pattern | Faster customer payment | Slower customer payment |

| Gross margin | Historical trend | Better mix or pricing | Cost creep or discounting |

| Hiring | Planned hires on schedule | Hires delayed until demand confirms | Hires still needed to support current work |

| Capital spend | Required investments only | Investments supported by cash | Purchases deferred unless critical |

Stress test the risks that actually hit established companies

The goal isn't to produce elegant scenarios. The goal is to expose weak points before they hurt you.

Start with the risks that are most common in mature founder-led businesses:

- Customer concentration: One major account slows payment or cuts volume.

- Project delays: Revenue shifts out, but labor and overhead stay in place.

- Margin compression: Supplier pricing, labor inefficiency, or discounting erodes gross profit.

- Working capital drag: Growth consumes cash faster than expected.

- Step-cost increases: A hire, facility expansion, or new system adds overhead before revenue catches up.

For construction, distribution, and professional services, this gets more useful when you tie the model to operational drivers. Track margin and cash conversion by job, client, or project. That's often where the damage starts.

If a single delayed receivable can force you to tap a line of credit, the issue isn't just collections. The issue is that your model wasn't built for the way cash actually moves.

This video does a good job reinforcing the shift from static budgeting to more active planning:

Use the model before you make the commitment

Most owners use financial reporting after the decision. That's backward.

Run the model first when you're considering:

- A key hire: Does the role pay off quickly enough, and can cash absorb the ramp?

- New equipment: Does the purchase increase throughput or margin enough to justify the cash hit?

- A large contract: Can you fund the working capital before customer cash arrives?

- A facility move or expansion: What does the fixed-cost increase do if volume comes in late?

Plain language works best here. Ask one simple question before each commitment: What happens to cash if this takes longer, costs more, or pays later than expected?

If the answer is “we'd be tight but okay,” you've got a manageable decision. If the answer is “we'd need to scramble,” you're not ready yet.

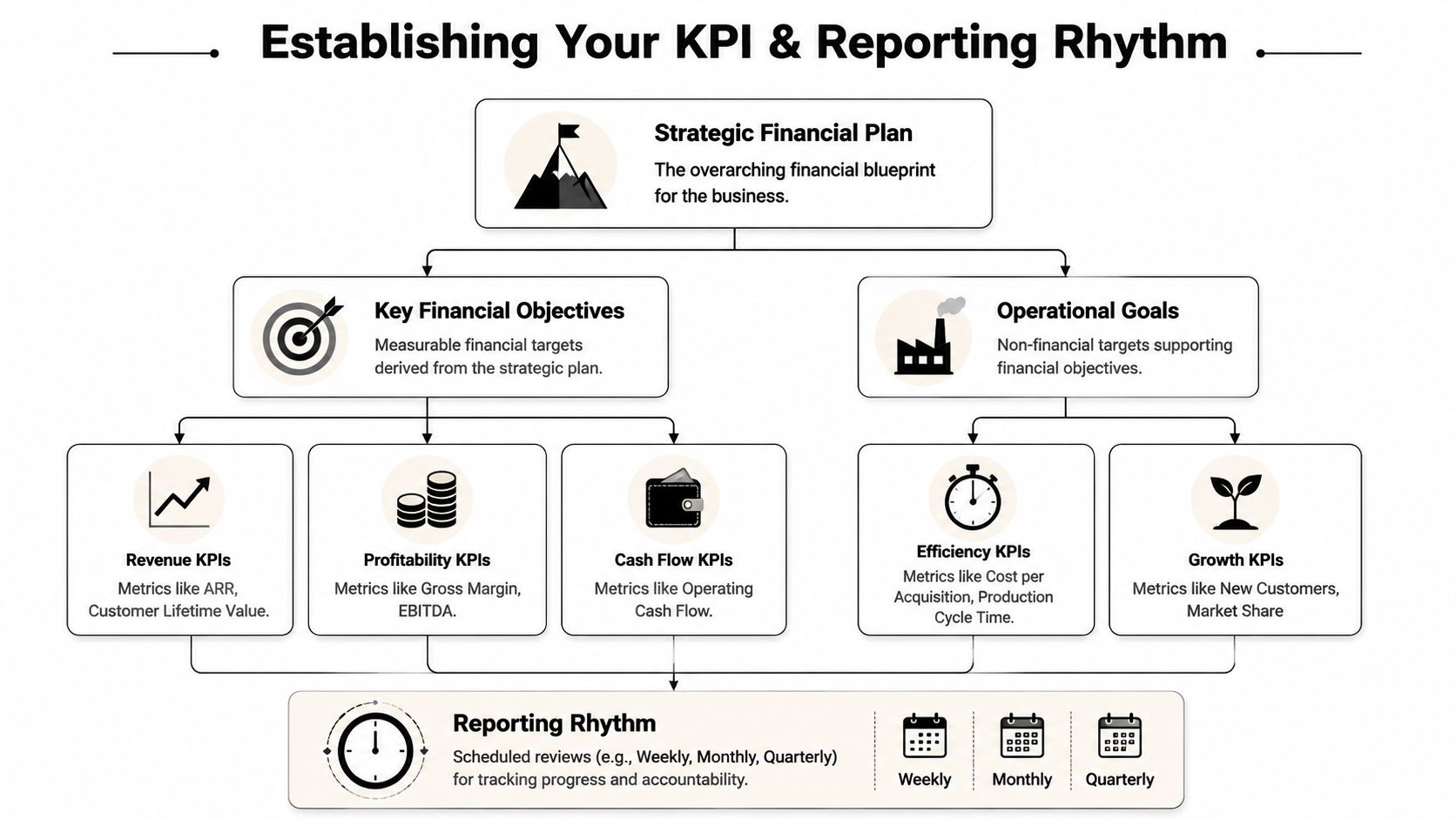

Establish Your KPIs and Reporting Rhythm

A plan without reporting is just a spreadsheet with good intentions.

Owners don't need more reports. They need a rhythm that forces action. If you review results only after month-end close, you're driving by looking in the rearview mirror. The business needs a tighter cadence and better signals.

Track leading indicators not just accounting results

Most companies overuse lagging indicators. Net income. Last month's revenue. Prior-period EBITDA. Those matter, but they tell you what already happened.

Leading indicators tell you what's coming. They give you time to act.

For a $10M to $100M business, your KPI set should include both:

Lagging indicators

- Gross margin: Shows whether core delivery is profitable.

- Operating profit: Tells you whether overhead is in line.

- Cash balance: Confirms current liquidity.

- Accounts receivable aging: Shows whether collections are slipping.

Leading indicators

- Pipeline quality: Not just total pipeline. Qualified, time-bound opportunities.

- Backlog health: Revenue scheduled and resourced to deliver.

- Utilization or crew productivity: A leading sign of margin quality.

- Quote-to-close pattern: Early warning of demand softness or pricing pressure.

- Work-in-progress exposure: Signals billing and cash conversion risk.

If you want a tighter view of which numbers matter most, this breakdown of the financial metrics every business owner should track is a practical companion.

Use a simple reporting cadence

You don't need a giant dashboard to create accountability. You need consistency.

A workable cadence looks like this:

| Review Timing | Primary Focus | Who Should Be Involved |

|---|---|---|

| Weekly | Cash, collections, sales movement, operational bottlenecks | Owner and key operators |

| Monthly | P&L versus plan, balance sheet changes, forecast update | Leadership team |

| Quarterly | Strategic goals, capital allocation, major risks, plan revisions | Owner and advisors |

That weekly review is where discipline gets built. Look at cash due in, cash due out, overdue receivables, and any major changes in pipeline or production. Then ask what decision must be made this week.

The best reporting rhythm is the one your team will actually keep. Short, sharp, and tied to decisions beats a beautiful deck nobody uses.

Build a one-page dashboard your team will actually read

If your dashboard takes twenty minutes to explain, it's too complicated.

A strong one-page dashboard should include:

- Cash section: Current cash, expected near-term receipts, expected near-term outflows.

- Revenue section: Actual versus forecast, open pipeline, backlog, billing pace.

- Margin section: Gross margin by business unit, customer, or job category.

- Working capital section: Receivables aging, payables pressure, inventory issues if relevant.

- Trigger items: Contracts at risk, customer concentration issues, hiring decisions pending, capex pending.

The discipline here isn't just for finance. It trains operations leaders, sales leaders, and project managers to understand how their decisions affect liquidity and profit.

That's when the financial plan stops being “finance's thing” and starts becoming how the company runs.

Implement Systems Controls Risks and Advanced Strategy

At some point, spreadsheets stop being flexible and start being dangerous. That usually happens right when the business gets complex enough that errors become expensive.

If you're managing multiple entities, locations, product lines, large projects, debt obligations, or owner transition plans, your financial plan for small business needs stronger systems and tighter controls. Not because software is magical. Because complexity punishes improvisation.

Upgrade the system before complexity beats you

Your accounting system records the past. Your FP&A process should help you manage the future.

That usually means separating three layers clearly:

- Accounting system for clean historical reporting.

- Forecasting model for planning, scenario analysis, and decision support.

- Management dashboard for fast visibility into KPIs and operating triggers.

If those three layers are mashed together in one giant spreadsheet with hidden formulas, you're taking unnecessary risk.

Use tools that fit your size and complexity. That might mean improving your ERP reporting, tightening job-cost or customer profitability data, or adding dedicated planning software. The specific product matters less than the discipline behind it. Clean data in. Standard definitions. Clear ownership. Controlled changes.

You also need controls that owners often ignore:

- Revenue recognition discipline: Don't let optimism pull revenue forward.

- Capex approval rules: Large purchases should tie back to forecast capacity and cash.

- Collections ownership: Someone must own overdue receivables every week.

- Margin review by unit of work: Job, client, route, or service line.

- Forecast version control: One current forecast, not five conflicting files.

Plan for shocks before they show up

Static annual budgets fail when reality gets noisy. Modern planning has to account for disruptions such as inflation, disaster exposure, and workforce issues, with more frequent forecast reviews and clear decision triggers, as discussed in Workday's guidance on creating a financial plan for your small business.

That means your plan should include responses to non-routine events, not just a base operating budget.

Build explicit triggers for decisions such as:

- Hiring: Add headcount only when backlog, utilization, or pipeline quality crosses a defined threshold.

- Equipment purchases: Commit only when production demand and cash support the purchase.

- Contract acceptance: Decline or renegotiate work if margin or payment terms create unacceptable cash strain.

- Reserve protection: Freeze discretionary spend if forecast cash falls below your minimum cushion.

Mature businesses distinguish themselves from reactive ones. They don't just track numbers. They pre-decide what action the numbers will trigger.

You should also review structural risks that don't show up neatly on the P&L:

- Customer concentration

- Supplier dependency

- Interest rate exposure

- Owner dependence

- Management bench strength

- Insurance gaps

- Weak contract terms

Operational discipline matters here just as much as finance. If your internal processes are chaotic, financial planning won't save you. It will just show you the cost of the chaos. This piece on turning your business into a well-oiled machine without losing your marbles is worth reading if the bottleneck is execution, not just finance.

Know when you need a fractional CFO

Plenty of businesses outgrow their bookkeeper and outside CPA long before they're ready for a full-time CFO. The question isn't whether finance matters. It's whether someone is actively owning forecasting, cash strategy, and decision support.

You likely need senior financial leadership if any of these are true:

- Cash is unpredictable: You're profitable, but bank balances still surprise you.

- Growth is stressing working capital: More sales are creating more strain.

- Margins are hard to explain: You know revenue, but not where profit is leaking.

- Major decisions are coming: Acquisition, expansion, debt restructuring, ownership transition, or exit prep.

- Reporting is slow or unclear: Leadership can't get a reliable view quickly.

- The owner is still the translator: Every financial decision routes through you because nobody else can frame the tradeoffs.

If the business is too complex for gut feel but too small for a full-time CFO, that gap will cost you more than you think.

Your Next Step From Plan to Profit

Don't overcomplicate the next move. Block time on your calendar this week and start building the plan from the ground up.

Use the first session to define the business outcome you're planning toward. Expansion. Debt reduction. Margin repair. Exit readiness. Then pull your historical financials and organize them by the drivers that matter in your business. After that, build the first-pass revenue, expense, and cash flow forecast. It won't be perfect. It doesn't need to be.

What matters is that you stop managing a $10M to $100M company with a mix of instinct, old reports, and whatever is sitting in the bank account today.

A financial plan for small business should give you control. It should tell you when to hire, when to wait, when to spend, when to push collections, and when a growth opportunity is worth the risk. If it doesn't do that, it's not a plan. It's paperwork.

If your company is in that awkward middle ground where the numbers matter more than ever, but you don't need a full-time CFO, AmbitionCFO helps founder-led businesses build cash flow visibility, forecasting discipline, margin insight, and exit-ready financial strategy without the cost of a full executive hire.